Why Bitcoin will succeed and reach $500k

Why Bitcoin will succeed and reach $500k

-

August 29, 2020

- Posted by: Farhad

Gold and oil have historically been reliable stores of value. Because they are scarce commodities, they make dependable hedges to the inflation of fiat currencies. As a result, they have commanded price premiums above and beyond the demand for their consumption alone.

For the last 75 years, the U.S. dollar has also been a reliable store of value. This is a result of its comparatively good management by the Federal Reserve and the strength, resilience, and reputation of the U.S. economy. In fact, it is the most widely held fiat currency in the world and recognized as the global reserve currency, denominating and settling the majority of international trade.

With that said, we believe there are fundamental problems with gold, oil, and the U.S. dollar as stores of value going forward. Below, we will make the case that bitcoin [1,2] is ultimately the only long-term protection against inflation.

[1] For clarification, Bitcoin capital “B” customarily refers to the overall Bitcoin network, whereas bitcoin, lowercase “b,” refers to the digital asset of the Bitcoin network (admittedly, this is confusing, especially when you have to rely on context alone in the case of starting a sentence with “Bitcoin”).

[2] Stylistically, we consider “bitcoin” an uncountable noun with no plural form. Similar to how there is no plural of “gold,” “bitcoin” is used whether we are referring to one bitcoin or more than one bitcoin.

The Problem with the U.S. dollar

Economic cycles are notoriously hard to predict, but, over a long enough time horizon, they do happen. The Keynesian tools that governments can avail themselves of to soften down cycles are well understood. Spending money, lowering taxes, and “printing money” (i.e., cutting rates, quantitative easing or “QE”, and/or adjusting cash reserve ratios for banks), are the major levers that governments can pull to counteract an economic contraction. These strategies, however, have diminishing returns and their ability to stimulate an economy depends upon how novel they are at the time they are being summoned.

Traditional wisdom dictates that during pro business cycles, a government should run a budget surplus — either by spending frugally, saving prudently, or some combination thereof — and print money sparingly. The idea is to have enough dry powder lying around to help jumpstart the economy if, and when, it starts to go into a tailspin. In practice, however, the U.S. government has been taking an entirely different tact. Even before COVID-19, and despite the longest bull run in U.S. economic history, the government was spending money like a drunken sailor, cutting taxes like Crazy Eddie, and printing money like a banana republic.

What began as a shot in the arm during the credit crisis of 2008, never stopped, despite the U.S. economy being out of the woods for years. And so what started as an acute prescription, has morphed into chronic dependence and denial (aka addiction). The resulting maladaptive behavior is, not surprisingly, very difficult to correct. See Exhibit A: every time the Fed tried to rein in QE pre-COVID, markets recoiled viscerally and became combative. And if stock market gains are your measure of success, you will choose not to upset the apple cart, even if it’s wildly untethered to reality. You will naturally avoid a painful intervention and rehabilitation and continue to kick the can down the road as long as you can.

According to the U.S. National Bureau of Economic Research, the U.S. recession that began in December 2007, ended by July 2009. Nevertheless, Treasury ran a budget deficit every year since, which in aggregate more than doubled Uncle Sam’s debt to $22 trillion dollars by the start of 2020. In addition, Treasury’s ability to collect money was attenuated in 2017 — Congress reduced the corporate tax rate from 35% to 21% by passing the Tax Cut and Jobs Act. Enter COVID-19. According to the Congressional Budget Office’s projections, the U.S. will run a deficit of $3.7 trillion in 2020 and $2.1 trillion in 2021, bringing the grand total to $29 trillion by September 2021 (cut to Ross Perot rolling over in his grave).

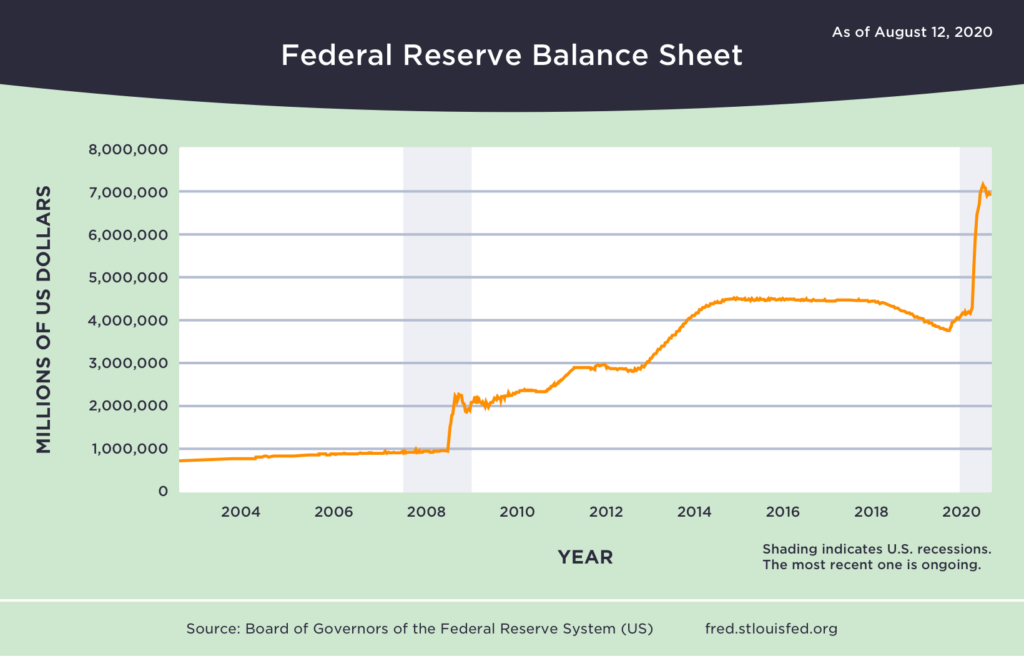

All of this pre-COVID excess was made possible through a combination of borrowing and printing. From July 2009 up to the pandemic, the line item for mortgage-backed securities on the Fed’s balance sheet grew approximately 3x from $545 billion to $1.6 trillion. Similarly, the book entry for Treasurys with a maturity date of greater than five years grew almost 3x from $315 billion to $872 billion. Together, these assets represent $1.6 trillion dollars printed out of thin air. They also demonstrate just how far the Fed wandered outside of its traditional mandate of promoting maximum employment and stable prices. While a central bank is expected to buy and sell short-term debt (Treasury bills or T-bills in the U.S.) in order to manage short-term interest rates, when it extends its open market activities to long-term Treasurys and other assets, it is operating firmly in the unconventional land of quantitative easing.

The increase in long-term Treasurys is perhaps the more troubling point. It reveals that one body of government (the Fed) has “purchased” $557 billion of debt from another body of government (the Treasury) using money it printed. By channeling its inner-Rumpelstiltskin and spinning straw into gold, the Fed bankrolled $557 billion dollars of the Treasury’s deficit spending. While technically there are intermediaries between the Treasury issuing these long-term Treasurys and the Fed purchasing them, the more this debt issuance-money printing merry-go-round turns, the more it looks and feels like self-dealing, or what economists would describe as unambiguous debt monetization — when a government finances its operations via the central bank’s printing press, as opposed to taxation and/or bona fide, arms-length borrowing.

Enter COVID-19, again. After pounding the turbo for more than a decade, the U.S. government was left with no choice but to pound it again. And practically overnight, the Fed waved it’s magic wand and increased the supply of U.S. dollars in circulation by $3 trillion.

Examining the The Fed’s balance sheet uncovers that it added $344 billion more mortgage-backed securities and $820 billion more long-term Treasurys (i.e., debt monetization) from February 2020 to July 2020. In other words, of the $3 trillion increase, $1.1 trillion was printed. To put this into perspective, the Fed printed two-thirds as much money in the last 6 months as it did over the prior 11 years. And that’s not all, the Fed has committed to a YOLO whatever it takes QE posture going forward…

On top of this, the House passed the CARES Act, authorizing a $2 trillion stimulus package that includes helicopter money (yes, Milton Friedman’s 1969 parable came to life in 2020) and lawmakers are currently negotiating another stimulus package. At the time of writing, House legislators are (gulp) “trillions of dollars apart.” Remember when a billion was a big number?

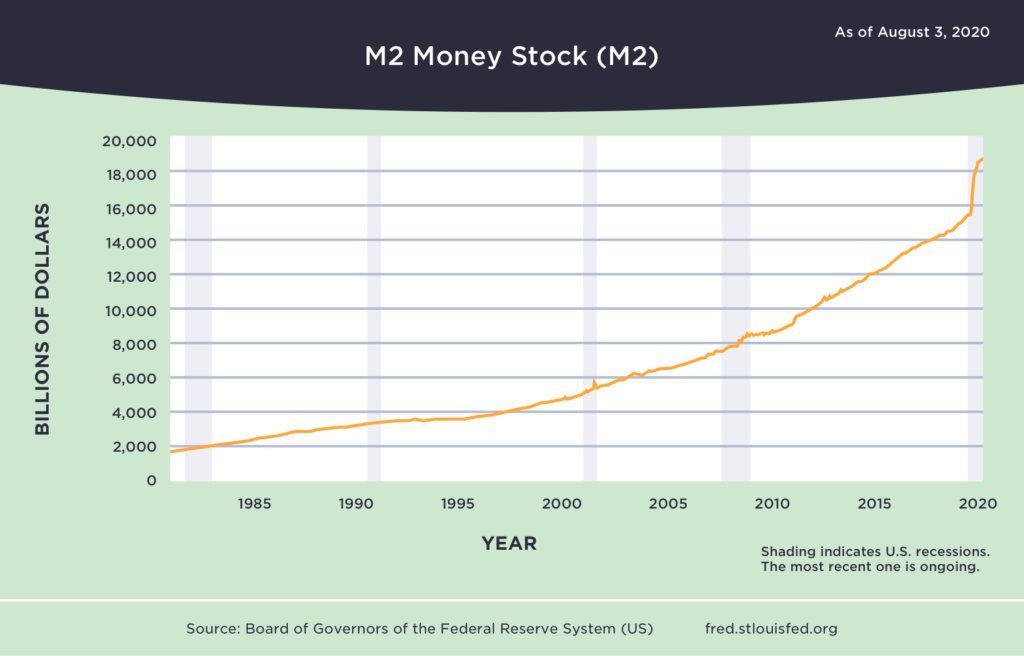

So what does all of this newly minted money mean? That the specter of inflation (or hyperinflation) is staring down on us. While inflation (as it is measured) remained under control over the past decade, the prices for luxury goods and assets, such as real estate (Bezos, Griffin, etc.), have arguably been inflating for some time. Pre-COVID inflation may have expressed itself in this way due to neo-liberal policies that favor Capital over Labor and because this money hose was extended primarily to “credit worthy” parties (think Wall Street, not Mainstreet), causing it to trickle up rather than down.

But COVID is a different story. While 2008 efforts were geared towards bailing Wall Street out of its self-created dumpster fire, the CARES Act is a $2 trillion dollar stimulus package designed to save the broader U.S. economy from a force majeure. It is aimed at Main Street and includes $300 billion of cash payments for individuals ($1,200 per person), $260 billion in additional unemployment payments, and $350 billion in small business loans. When these checks get cashed, they won’t be spent on trophy mansions in Bel Air, but instead on core goods such as bread, milk, and razor blades, injecting cash directly into the major arteries of the U.S. economy. While it’s too early to tell whether these stimulus acts will simply fill a hole of otherwise lost income or have a much larger impact on prices, we are no doubt sailing in uncharted waters.

The Great Monetary Inflation is nigh.

If You Wanna Dance, You Gotta Pay the Fiddler

The world is drowning in debt. And this was the pre-pandemic consensus.

COVID’s impact has been so swift and blunt that it can easily distract from the fact that it’s actually just another layer on a global debt cake that has been baking for quite some time. And the layers of this cake involve structural problems that don’t go away with a vaccine. From 2009 to 2019, the U.S. debt-to-GDP ratio swelled from 83% to 106% — post-COVID it’s on track to hit 135% by September of this year. To bottom-line this, the U.S. debt-to-GDP ratio will grow more this year than it did over the entire prior decade. China’s debt-to-GDP ratio was 300% entering COVID and has grown to 318% as of Q1 2020. The rest of the world is not faring any better.

Taking the COVID goggles off, unfavorable tectonic demographic shifts have been well underway in many developed countries for decades. Falling birth rates have inverted population pyramids, which means that shrinking younger generations will increasingly be unable to shoulder the growing debt burdens (e.g., healthcare, pension, social security, etc.) that have been handed down to them by the much larger, older generations. In Japan, this demographic challenge is best illustrated by the fact that more adult diapers are sold in a year than baby diapers.

Putting the COVID goggles back on, the pandemic is bringing this dance with debt closer to its inevitable finale. And it’s severely limited the efficacy of responses available to governments when the next black swan lands. The Keynesian standbys of increasing spending and lowering taxes have become threadbare and haggard. We’re reaching a point where creating more debt to stimulate the economy, in the context of so much existing debt, won’t work. While the third and final lever, cutting rates, is out of bullets because short-term interest rates are already at or below rock bottom (negative in some instances).

Sooner or later, these ballooning debt-to-GDP ratios will begin to strain credibility (if they haven’t already) and the fiddler will hold out her hat. At the risk of mixing metaphors, there will be no choice but to face the music. The younger generations will awake to the generational plunder that has been bestowed upon them and be forced to atone for the sins of their mothers and fathers.

Printing Out of Debt

When the day of debt reckoning comes, governments will have several options available to reduce their debt, none of which are pretty. They can choose to (i) not pay some portion of their debt (i.e, “hard default”), (ii) adopt austerity measures in hopes of running a budget surplus, or (iii) reduce the value of the debt they owe through inflation (i.e., “soft default”).

- A Hard Default is highly undesirable as it generally leads to further crisis and calamity, not less. Given the fact that the U.S. dollar is the global reserve currency, a hard default by the U.S. government on any amount of its debt would be catastrophic to the global economy. It is, therefore, hard to imagine any future in which the U.S. government would hard default on any portion of its debt.

- Austerity measures face their own set of challenges. Implementing them requires a strong political will and an even stronger stomach. The U.S. government has run a budget surplus only four times in the last 50 years. When a government actually tightens its belt and chastens its spending, it is often greeted with riots and insurrection. In addition to fomenting social unrest, spending cuts and tax increases tend to shrink GDP, further aggravating debt-to-GDP ratios and making an already bad situation worse.

- A Soft Default is the likely strategy for most governments trying to deleverage, including the U.S. government. And just this morning, Fed chairman Jerome Powell inasmuch confirmed this. In this scheme, a government intentionally devalues its currency in order to erode the real value of the debt that it owes. Lenders still get paid the same amount of dollars that they are entitled to, however, because of inflation, such dollars are now worth less in real terms. Economic studies show that this approach produces less damaging long-term outcomes than a hard default, whereby lenders get paid less dollars than they are entitled to or no dollars at all.

When a central bank elects to pursue a soft default strategy, it targets a particular inflation rate and proceeds to print enough money to hit it. Once reached, this target inflation rate reduces a government’s debt obligations by the same rate. And while the stated reason for the COVID money printing spree may have been economic stimulus, its input and end result will be the same; a rose by another name. Regardless of the rationale, an increase in the money supply relative to the available goods will always lead to a rise in prices, which is to say inflation.

How a government distributes newly minted money is an interesting policy issue that can determine where inflation rears its ugly head (see earlier thoughts on ‘trickle up’ inflation). If the government is the recipient, then the soft default is considered debt monetization or the nationalization of debt. If both depositors and borrowers get it — depositors through higher interest rates and borrowers through lower interest rates — then it’s called dual interest rates. If lenders and shareholders get it, then it’s quantitative easing. If the people get it, then it’s helicopter money, and so on.

Winners and Losers

Regardless of what channel the central bank uses to inject money into the economy, the winners and losers are the same: borrowers will be rewarded at the expense of lenders and depositors. Investors and entrepreneurs will be more able to adapt to rising prices, while those who are tied to fixed cash income (e.g., civil servants, Social Security recipients, pensioners, etc.) will share the same fate as lenders and depositors. Ultimately, inflation damages trust and will make it harder and more expensive for a government to borrow the next time around. Depending on how long or short memories are, this trust could take generations to rebuild.

And while COVID has hurled us further down the path towards a soft default, the greater culprit is the U.S. government’s permanent and unapologetic policy shift towards a debt-monetization model to finance its operations. Central banks have seen this coming for some time and have been bracing themselves. If there ever was a time to hedge against systematic fiat currency risk, that time has come.

The Problem with Oil

Oil is no longer a reliable store of value. Supply. Technological advancements in fracking have dramatically increased the supply of oil and have called into question the Hubbert peak theory and other peak oil theories. It turns out there is much more oil underground than anyone ever thought. Demand. In addition to oil becoming more plentiful, there are global forces at play reducing its global demand, such as the push for renewable energy and the political pressure in many countries to reduce carbon footprints.

Storage. Oil’s physical nature combined with its large industrial application makes it uniquely vulnerable to sudden and severe negative demand shocks. When demand dries up, oil that would have otherwise been consumed, must be stored. This is normally not a problem, unless a demand shock is so steep and abrupt that it’s resulting supply glut overwhelms the available storage infrastructure. Because storage is so inelastic, such a scenario can lead to a gnarly game of musical chairs. And that’s exactly what happened on April 20th, a month into the U.S. pandemic lockdown. Demand for oil dropped so precipitously that oil holders suddenly found themselves scrambling for storage depots. When storage ran out, those still holding barrels had no choice but to pay people to take their oil, causing the price of oil to go negative. Yes, really, the West Texas Intermediate oil benchmark closed at -$37.63.

The Problem with Gold

Currently, gold is a reliable store of value and the classic inflation hedge. Supply. The supply of gold is actually unknown. While gold remains scarce or “precious” on planet Earth, the same cannot be said with respect to our galaxy. Scientists believe that asteroids contain a plethora of metals, including gold, and have compiled a database of over 600,000 asteroids and their compositions.

Commercial asteroid mining may sound like science-fiction, but the ‘Space Gold Rush’ has begun. NASA’s mission to explore the metal asteroid Psyche will commence in 2022 and, in an effort to incentivize space entrepreneurship, the U.S. government has already enacted legislation that allows asteroid mining companies to own whatever they mine from asteroids, or otherwise obtain in space. And since 2016, the UN’s Committee on the Peaceful Uses of Outer Space has included space resources as agenda item 15 on its Legal Subcommittee. If technological advancements progress over the coming decades to allow for practical and reliable access to near-Earth asteroids, it could lead to a massive, positive supply shock in the market for gold.

Elon Musk already plans to put humans on Mars (including himself) and recently won the contract to launch the aforementioned NASA Psyche mission. Since 1997, NASA has successfully landed four rovers on Mars. It seems entirely plausible that Elon Musk, the founder of a private aerospace company (SpaceX) and a tunnel construction company (The Boring Company), will be able to put a machine on an asteroid, drill a hole, and retrieve the extractions back to earth within his lifetime. Even a semi-credible effort that foreshadows this long-term inevitability will crater the price of gold.

Portability. It’s hard to move gold in the middle of a pandemic. It’s hard to move gold during a war. It’s hard to move gold if there’s a change in government attitude towards your property rights. It’s hard to move gold, period. If you’ve ever seen Die Hard with a Vengeance, you know it can take dump trucks to move gold.

The Answer

We’ve laid out the problems with the U.S. dollar, oil, and gold. Now let’s talk about the solution. But first, let’s establish a few general ideas and some perspective on money:

- Money is a technology. It was first invented thousands of years ago to solve for the limitations of barter; namely what economists refer to as the coincidence of wants dilemma.

- Like any technology, money can always be improved upon and iterated on. Humans have been evolving money since its inception, crypto is just the latest iteration.

- Money has been many things over the years, including, but not limited to, shells, beads, metal, paper backed by metal, paper not backed by metal, and much more. Ultimately, money is whatever we all agree it is.

- Bitcoin is the world’s first Internet-native money, which is to say: money purpose-built for the Internet. It works the same way that your email works, which is not the case for all other forms of money.

- Cryptocurrencies like Bitcoin are networks (not companies) and should be valued using Metcalfe’s Law. Methods used to value companies, such as discounted cash flow models, simply won’t work. Even drawing stock market bubble analogies is comparing apples and oranges.

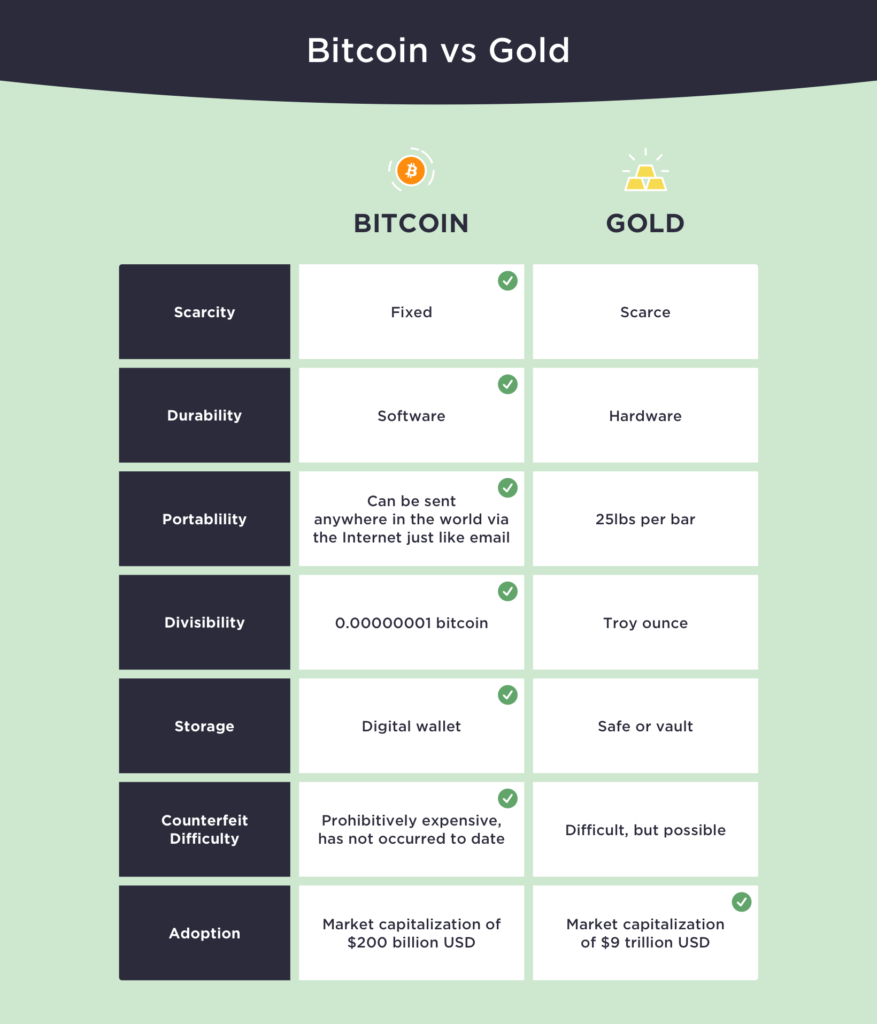

Now back to the solution. While Gold is the classic inflation hedge, there are compelling reasons why bitcoin is poised to take its mantle. Supply. Bitcoin is not just a scarce commodity, it’s the only known commodity in the universe that has a deterministic and fixed supply. As a result, bitcoin is not subject to any of the potential positive supply shocks that gold (or any commodity for that matter) may face in the future.

Beyond superior supply attributes, bitcoin possesses all of the other characteristics that make gold valuable and actually performs better on a side-by-side comparison.

As it turns out, bitcoin is better at being gold than gold — and not just incrementally, but by an order of magnitude or 10X better. It is a widely held belief in technology circles that when a product is 10X better than its closest substitute, it will escape its competition. We believe Bitcoin has achieved this. Portability. For example, Bitcoin works like your email, which means it’s borderless and never sleeps — any amount can be sent anywhere in the world over the Internet, 24/7/365. This makes it not just very portable, but also very censorship resistant (e.g., blockades, seizures, etc.). It’s not hard to move bitcoin in the middle of a pandemic, a war, or a change of government. It’s easy to move bitcoin, full stop.

Breakthrough. How was this all made possible? Prior to the invention of Bitcoin, the idea of a decentralized network of money, in which unrelated computers around the world could reliably reach agreement with each other, was thought to be entirely theoretical. How could strangers agree on who owns what and ensure that people don’t spend more than they have when there is a clear incentive to try and cheat the system?

In computer science, this problem of agreement is known as The Byzantine Generals’ Problem. In the context of the money, it is referred to as the double-spending problem. When Satoshi Nakamoto, Bitcoin’s pseudonymous creator, published the Bitcoin white paper in 2009, she, he, or they presented the world’s first ever solution to this intractable agreement problem. Behold the Bitcoin mining algorithm. As described, it ensures that a network of computers that don’t know each other will in fact reach agreement with each other in a reliable manner. And that this agreement or consensus — what today, we call a blockchain — would be immutable and verifiable.

Historically, such agreement had to be entrusted to a central party or ended up concentrating towards one. For the first time in the history of the world, this is no longer the case. The magnitude of this breakthrough cannot be overstated. It is easily as significant as the invention of the Internet itself.

Network Effects. With respect to other cryptos, Bitcoin has a significant first-mover advantage not only because it’s the first crypto as we know it, but because it was the first one with gold-like store of value properties. As such, it enjoys tremendous network effects (not dissimilar to those experienced by social networks like Facebook and Twitter) due to its vibrant community of users, developers, miners, exchanges, custodians, etc. Nothing demonstrates this better than the fact that Bitcoin is an open-source project that can be copied or forked by anyone in the world at any moment. And yet despite being forked many times over the years, it remains the dominant crypto (store of value or otherwise) both in terms of market capitalization and liquidity. This race is Bitcoin’s to lose.

To the Moon

Inflation is coming. Money stored in a bank will get run over. Money invested in assets like real estate or the stock market will keep pace. Money stored in gold or bitcoin will outrun the scourge. And money stored in bitcoin will run the fastest, overtaking gold.

It’s true that gold has a multi-millenia head start and strong foundation of trust. As a result, it may be the right short to medium-term choice for risk-averse types. Afterall, Bitcoin is still young and therefore carries both significant technological risks as well political risk in certain jurisdictions.

Nonetheless, we believe that bitcoin will continue to cannibalize gold and that this story will play out dramatically over the next decade. The rate of technological adoption is growing exponentially. Software is eating the world and gold is on the menu.

Bitcoin has already made significant ground on gold — going from whitepaper to over $200 billion in market capitalization in under a decade. Today, the market capitalization of above ground gold is conservatively $9 trillion. If we are right about using a gold framework to value bitcoin, and bitcoin continues on this path, then the bull case scenario for bitcoin is that it is undervalued by a multiple of 45. Said differently, the price of bitcoin could appreciate 45x from where it is today, which means we could see a price of $500,000 U.S. dollars per bitcoin.

All of this does not factor in the possibility of bitcoin displacing some portion of the $11.7 trillion dollars of fiat foreign exchange reserves held by governments. Foreshadowing this, at least one publicly-traded U.S. corporation has begun holding bitcoin as a treasury reserve asset. If central banks start to diversify their foreign fiat holdings even partially into bitcoin, say 10%, then 45x gets revised upward towards 55x or $600,000 USD per bitcoin, and so forth.